A turnover declaration is a key part of managing your credit insurance. At the end of your policy period, you’ll report the actual value of your insurable sales or revenue generated during that time. This allows us to adjust your premium, if needed, so it accurately reflects your business’s activity.

By submitting an accurate turnover declaration, you can make sure you’re only paying for the coverage you need — no more, no less. Here’s how it works:

If your sales exceeded the estimated turnover, we’ll calculate any extra premium based on the actual figures, and you’ll be invoiced for the difference.

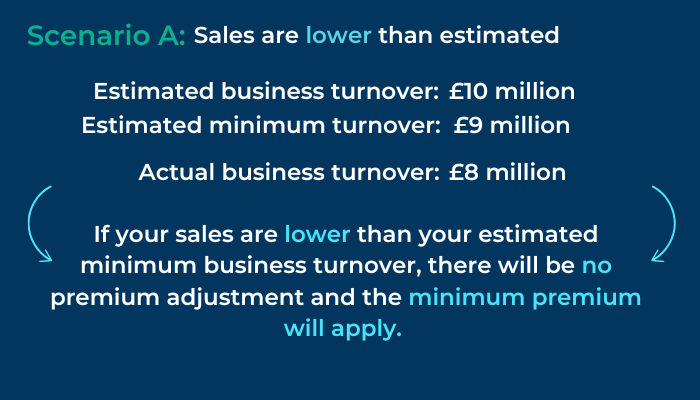

If your sales were lower than your estimated minimum turnover, there’s no premium adjustment; you’ll simply pay the minimum premium you agreed upon*.

In cases where you have a fixed or flat premium, your premium won’t change at all, regardless of your turnover declaration.

Submitting a turnover declaration may seem like a small administrative step, but it can make a big difference in ensuring your insurance coverage is both accurate and cost-effective.

Why is this important?

Your premium is calculated based on several factors, including your estimated insurable turnover. When we issue your policy, we charge a minimum premium upfront, typically around 90% of the estimated total, which can be paid in installments throughout the insurance period. However, if you have a fixed premium rate, this won’t change.

By submitting your turnover declaration, you ensure that you’re paying the correct premium based on your real business performance. This helps you avoid unexpected costs, stay compliant, and—most importantly—keep your coverage uninterrupted. Regularly updating your turnover also gives you peace of mind, knowing your insurance is accurately aligned with your business needs.

Example

See below example of how Coface estimates your insurance premium.

Using the above example and to help calculate your turnover declaration, see the below scenarios.

Scenario A:

Scenario B:

Submitting these declarations is essential, as failure to do so results in a breach of policy, which can lead to suspension of cover and may give us the right to terminate the policy.

What you need to do

At the end of your policy period, you must log into Cofanet to complete your turnover declaration. Key information to include would be:

Value of goods and/or services sold:

Report all business conducted during the specified dates. This should reflect the full insurable turnover of your company and any affiliates on your policy and ensure the currency input is correct.

Countries:

Declare turnover for each country endorsed to your policy. For adding new countries, please contact our Client Services at +44 0800 0856 848 (UK) or +353 12304669 (Ireland).

Breakdown of figures:

For UK businesses, separate UK local sales and UK indirect exports (sales where goods are exported immediately and treated as exports for insurance premium tax purposes).

If there are affiliates on the policy, combine their sales with yours on Cofanet.

What to exclude:

- Sales not covered by your policy, such as pro-forma payments, sales to subsidiaries or associate companies, sales to public sector organisations. and sales to public customers (unless explicitly covered).

- Sales made to insured customers after coverage has been refused or withdrawn and upon expiry of your Grace Period/Binding Order Period

- VAT, unless specifically covered under your policy.

By accurately completing the Turnover Declaration, you help maintain the integrity and accuracy of your policy; if you have questions or need assistance, please reach out to your designated Account Manager.

*Subject to policy terms and conditions, subject to insurance premium tax (IPT).